Podcast: Play in new window | Obtain

We had a actually just right run with the inventory marketplace over the last 10+ years. It looked like the marketplace used to be on a continuous race to better and better ranges. If truth be told, many hobbyist buyers made impossible fortunes by way of launching blogs and meting out funding recommendation that in large part parroted the long-standing ethos of the now past due Jack Bogle. And so they seemed like geniuses till very not too long ago.

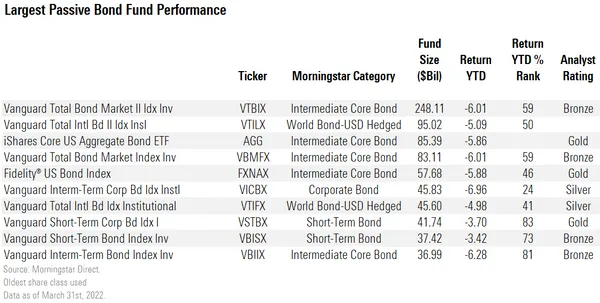

Now everyone seems to be having a look to diversify menace and in finding property that can protect them from marketplace volatility that may not move away. Bonds don’t seem to be running. In step with Morngingstar, the ten greatest bond finances misplaced a median of five.42% within the first quarter of 2022.

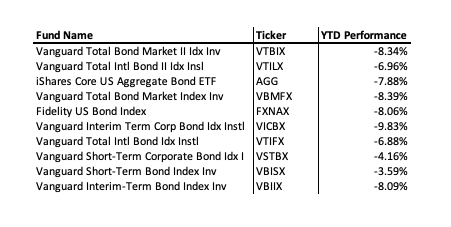

And if we have a look at this similar number of finances, we discover that efficiency worsened since Q1 of this yr:

Now the typical nominal decline amongst all of the finances is -7.22%. It does stay true that bonds seem more secure than the full inventory marketplace. The use of the S&P500 Index as our measuring stick, it is down round 12.62% YTD.

Existence Insurance coverage, the Actual Flight to Protection

The use of both complete lifestyles insurance coverage or listed common lifestyles insurance coverage as a buffer in opposition to volatility is one thing we now have been doing for a couple of many years. I am not having a look to make an “us vs. them” argument that seeks to persuade any individual that they must in an instant promote all in their shares/bonds and purchase up as a lot lifestyles insurance coverage as that can permit. That is idiotic and hasn’t ever been the placement we take right here at The Insurance coverage Professional Weblog.

What I do need to argue these days is that you’ll be able to use lifestyles insurance coverage as a approach to de-risk your portfolio with nice luck in the event you practice the correct trail.

First, let me indicate that lifestyles insurance coverage (apart from variable lifestyles insurance coverage merchandise) is an overly low or 0 volatility product relating to year-over-year account values. It is engineered to ensure in opposition to losses, and there’s a multitude of advantages this presents you. Nowadays is not the day we will be able to element each unmarried a kind of advantages, however I need you to carry directly to that concept as we unpack the remainder of this dialogue.

And since it is extraordinarily tough to really take hold of what a monetary made from any sort has to provide when mentioned purely within the theoretical sense, I can as a substitute use some examples to extra explicitly name out what precisely lifestyles insurance coverage has to provide.

De-Risking Your Portfolio with Entire Existence Insurance coverage by way of Transferring Belongings to Existence Insurance coverage

Let’s take a look at the next state of affairs. Male, age 50 who has amassed a pair million bucks in property. He is heading in the right direction referring to retirement preparedness, however he worries about losses bringing his amassed property down. He understands that simply because he is accomplished a definite steadiness prior to now, shares and bonds can’t make it possible for his portfolio will at all times be price what it’s these days or extra.

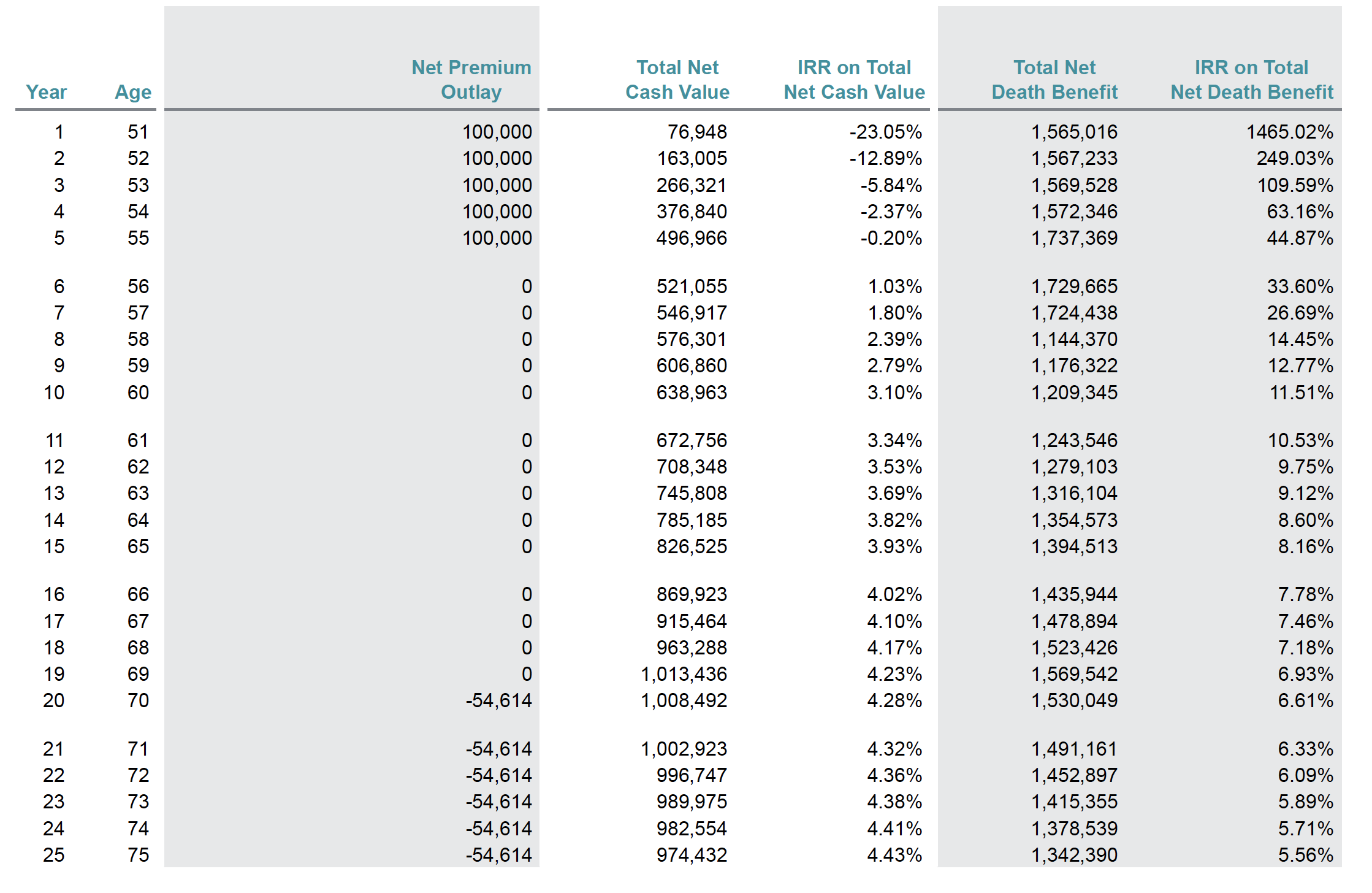

He’s going to promote $500,000 price of property and transfer it to a complete lifestyles insurance coverage. This coverage makes use of a number of complicated design tweaks to be sure that it provides the best imaginable stage of money worth accumulation whilst minimizing much less necessary choices from the insurance coverage corporate (specifically loss of life receive advantages).

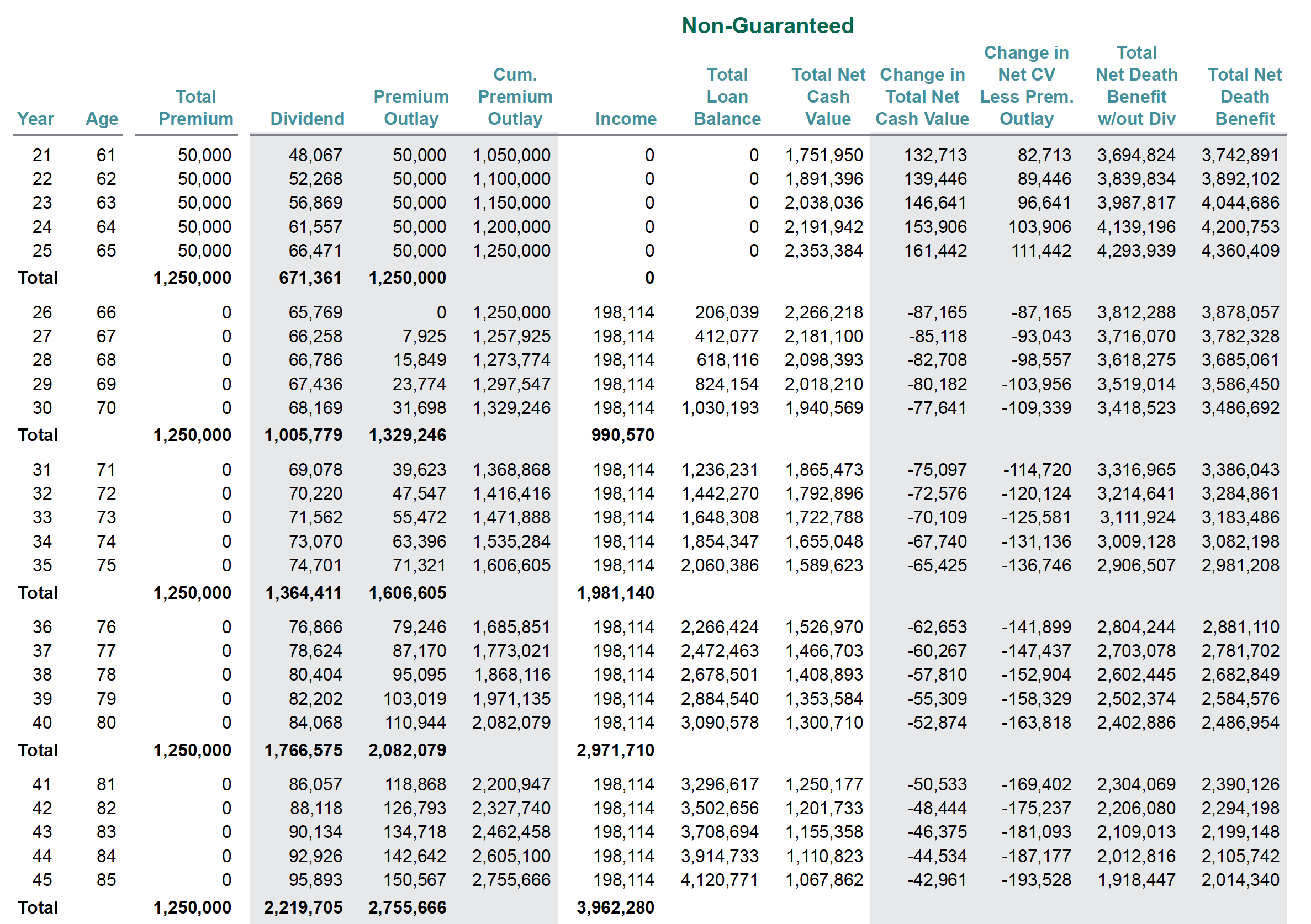

Here is a ledger that initiatives what he’s going to succeed in with this transfer:

Realize that by way of 10 years out, he has accomplished a three.10% go back on his cash. That is an overly sexy consequence for an asset with a nil likelihood of turning damaging. This consequence will get even higher come yr 20 when the result’s 4.28%. However the fee of go back is an continuously deceptive determine and it manner not anything in most cases talking when having a look to make use of the cash for day by day residing bills.

At yr 20, he can take an source of revenue of just about 5.5% of the account steadiness, and maintain this source of revenue all of the solution to age 100 (no longer pictured within the ledger above). This source of revenue is freed from source of revenue taxes, no longer matter to Changed Adjusted Gross Source of revenue calculations, and fully versatile. Once I say versatile, I imply he is not compelled to take any certain amount underneath any particular time-frame–like an annuity receive advantages or dividend funding may require.

The facility to take an source of revenue by contrast asset this is relatively a little upper than the standard 4% advice comes from the loss of volatility within the asset. The truth that this coverage won’t ever enjoy a yr the place the speed of go back on money worth is damaging presents the landlord higher withdrawal energy. The speed of accumulation may range, however that has a considerably lesser have an effect on on distributable source of revenue than the timing of damaging returns.

Understand that he nonetheless owns over 1,000,000 bucks price of shares that can expectantly develop at a fee commensurate with commonplace inventory marketplace returns. The entire lifestyles insurance coverage play simply locks in a specific amount of asset worth to carry peace of thoughts in opposition to long run volatility within the inventory phase of the portfolio.

Additionally, it’s a must to be aware that that is all scalable in both path. If he had extra property and sought after a bigger quantity going to lifestyles insurance coverage or if he had fewer property and put much less into lifestyles insurance coverage, the relative effects are very equivalent. I merely carry this as much as indicate that in case your state of affairs is other, that does not exclude you as a candidate for the sort of technique.

However there’s a other way which may be the easier choice for many of us.

Atmosphere the Level to De-Chance within the Long run

Now let’s check out a special situation. 40-year-old who’s beginning to concern about what dangers he may face as he attracts closer to retirement. He has stored a tight quantity thus far, however he is questioning if he must tweak his method to deal with long run dangers proactively. He’d moderately depart the property he does have available in the market and benefit from what that can most probably produce over the following couple of many years.

He will take $50,000 from the volume of his annual financial savings and use it in a complete lifestyles insurance coverage. Usually, insurance coverage brokers may display him a situation very as regards to this one:

That is completely advantageous and can paintings relatively neatly as a retirement source of revenue asset. However we will be able to make a couple of tweaks that probably produce much more purchasing energy from this asset, however coordinating it along with his different property as a de-risking technique.

We all know he will gather wealth via different property past simply this complete lifestyles coverage. So what if he took a few of the ones property and moved them to a much less dangerous allocation inside lifestyles insurance coverage as he enters retirement?

The source of revenue projection above assumes a number of issues about the entire lifestyles coverage. It assumes a definite dividend. It assumes that the coverage proprietor will take source of revenue to age 100 after which quit. It additionally assumes that the mortgage used to generate this source of revenue will gather pastime each and every yr and that pastime might be added to the mortgage steadiness–i.e. no longer paid by way of the coverage proprietor.

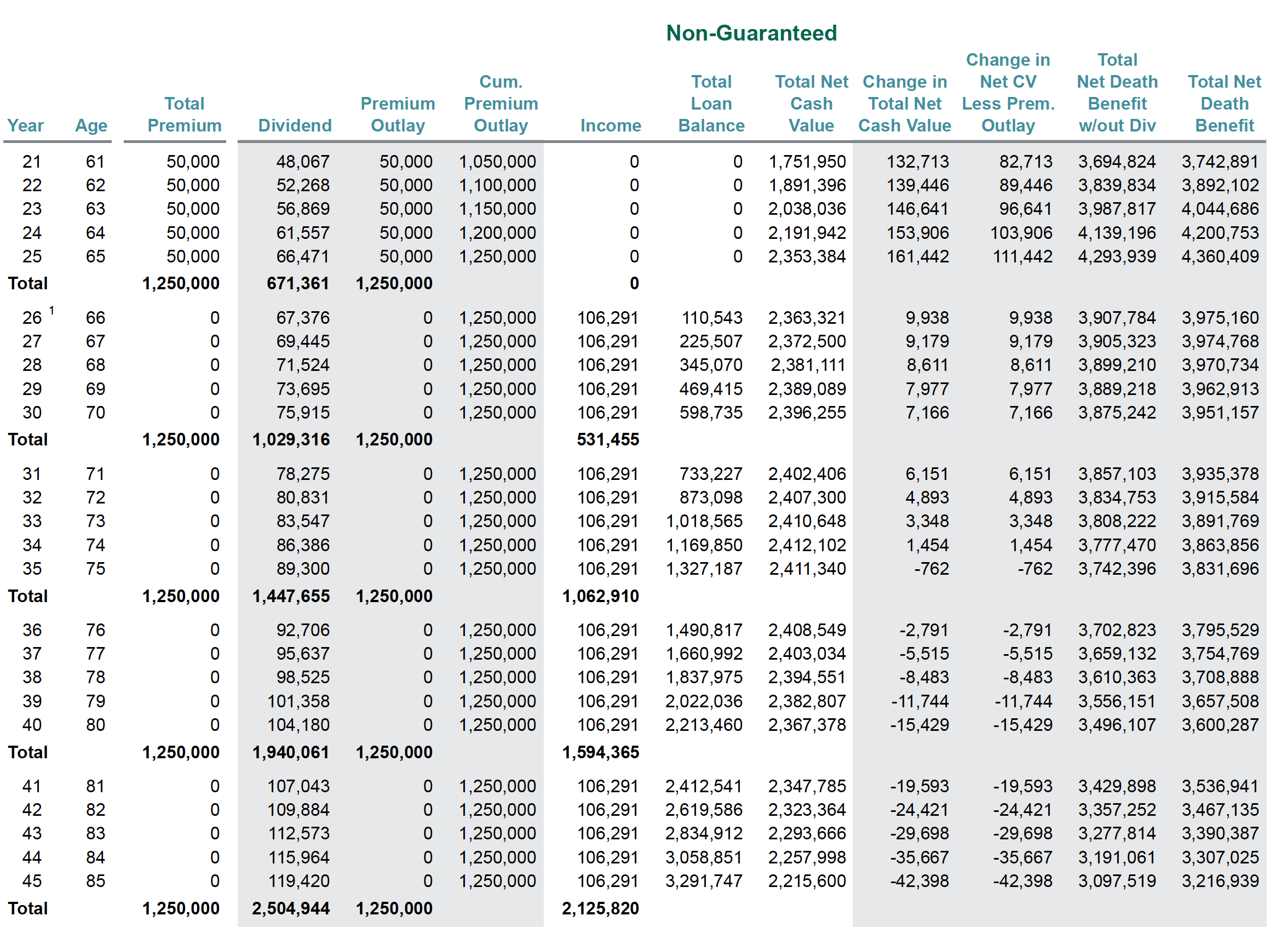

However what if he did pay the mortgage pastime? What if he took some cash from his different property and made an pastime cost each and every yr? That is what occurs:

He features virtually $92,000 according to yr in source of revenue. He accomplishes this by way of successfully shifting a few of his riskier property into complete lifestyles insurance coverage via mortgage compensation, thus offering himself having the ability to fortify the extra strong and non-taxable source of revenue he gained from his complete lifestyles insurance coverage. Realize that all through the primary 5 years he will pay a complete of $79,246 in mortgage pastime and features $459,115 in source of revenue. That is a candy tradeoff.

Call to mind it like this, the source of revenue delta right here is precisely $91,823. Which means if he will depart cash in his different property, he must ensure that he can generate a minimum of that a lot source of revenue–or regardless of the an identical worth to him is–according to yr by way of leaving the cash within the different property.

Understand that lifestyles insurance coverage lacks volatility making its source of revenue era features very robust in opposition to different property. Additionally, do not disregard that lifestyles insurance coverage source of revenue figures are web of the whole thing–e.g. taxes and charges.

Although he selected to prevent promoting off different property to pay the lifestyles insurance coverage mortgage pastime one day, he may just nonetheless generate extra source of revenue than the unique $106,291. It is at this level that numerous folks gets caught on what’s the exactly right combination. How a lot of my different property must I re-deploy into lifestyles insurance coverage as I am getting older to fortify my source of revenue? That is an unknowable resolution, and you should not torture your self with it. The purpose of this concept experiment is not to turn out simple the precise way one must absorb all cases. It is to show what is to be had. To lend a hand folks notice simply what choices they’ve at their disposal after they incorporate lifestyles insurance coverage into their portfolio. And most significantly, how robust an impact lifestyles insurance coverage merchandise have on minimizing menace when they’re used on this model.

And you already know what else? There are much more choices than you can most probably understand by way of studying this right here article. And that’s the reason an excellent matter for any other day.